It would be interesting to see if any NYSE listed companies would be interested to list on the JSE. Picture: Timothy Bernard

Listing is fast becoming the flavour of our time. There’s blacklisting (banks install the fear of life on their clients), Grey listing, (the international community threatens South Africa to come in line), a Red list of endangered species, (if you get on this list, you are likely to get extinct), and enlisting - to go to war in Russia.

The list goes on, and now we have the dual list.

Hopefully, this is a good list.

The New York Stock Exchange, part of Intercontinental Exchange, Inc. (NYSE: ICE), and the Johannesburg Stock Exchange (JSE) recently announced the signing of a Memorandum of Understanding to collaborate on the listing of companies on both exchanges.

The United States ranks as one of South Africa’s largest trading partners and the MoU is designed to help support the economic relationship between the two nations.

Today, about 600 U.S. companies operate in South Africa in sectors including manufacturing, technology, finance, insurance, and wholesale trade.

It would be interesting to see if any NYSE listed companies would be interested in listing on the JSE.

A dual-listed company or DLC (also referred to as a Siamese twin) is a corporate structure which involves two listed companies with different sets of shareholders, sharing ownership of one set of operational businesses.

A dual listing of a company is a way for a company to have two equal listings (neither being a secondary) in different markets. Companies use dual listings because of their benefits which include additional liquidity, increased access to capital, and the ability for their shares to trade for longer periods if the exchanges on which their shares are listed are in different time zones.

Companies with dual listings include Investec- listed in SA and the UK, Unilever listed in the UK and the Netherlands, the Mondi Group and Rio Tinto listed in Australia and the UK.

The main advantage of a dual listing is the access to additional capital and increased liquidity. Considering exchange rates and other complications, stock prices should remain the same on both exchanges.

If not, an arbiter will bring them together. A dual listing, also known as inter-listing or cross-listing, is attractive to many non-U.S. companies because of the depth of the capital markets in the US, the world’s biggest economy.

The NYSE and the JSE have also agreed to jointly explore the development of new products and share knowledge around ESG, ETFs and digital assets.

This aspect of the agreement may benefit the South African investment space the most.

The NYSE Group is a subsidiary of Intercontinental Exchange (NYSE: ICE), a leading global provider of data, technology, and market infrastructure.

Intercontinental Exchange, Inc. (NYSE: ICE) is a Fortune 500 company that designs, builds, and operates digital networks to connect people to opportunity. Trademarks of ICE and/or its affiliates include Intercontinental Exchange, ICE, ICE block design, and New York Stock Exchange.

This new blockchain, called ICE, will bring about a new application hub for the ICON ecosystem. With ICON, you will be able to wrap assets, natively swap assets using each respective network’s underlying security, query data between networks and much more.

The South African Regulators will also have to hone their knowledge and skills.

A foreign company may seek an ordinary listing, the most prestigious type of listing, on an exchange such as the NYSE or NASDAQ, but the requirements to do so are stringent.

In addition to meeting the exchange’s listing criteria, the foreign company must also satisfy US regulatory requirements, restate its financials, and arrange for clearing and settlement of its trades.

Among the drawbacks is that dual listing is expensive due to the costs involved in the initial listing and ongoing listing expenses. Differing regulatory and accounting standards may also necessitate the need for additional legal and finance staff.

Dual listing could place more demands on management as well, given the additional time required to communicate with investors in the second jurisdiction through roadshows, for example.

The level of development of South Africa’s financial sector infrastructure is an important contributor to the sophistication of the financial market overall.

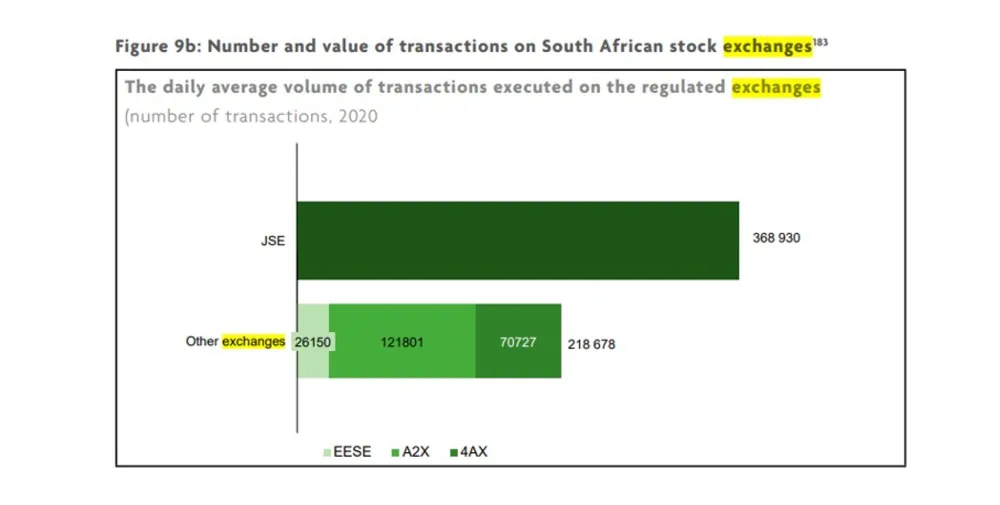

The financial sector infrastructure landscape consists of five exchanges, two central securities depositories (CSDs) and two clearing houses regulated by the FSCA.

Of the five registered exchanges, four are currently active and one exchange, namely ZARX, is undergoing liquidation. The Johannesburg Stock Exchange (JSE) has operated as the only exchange in South Africa for the bulk of the last 129 years. The South African Futures Exchange (Safex) – trading financial and commodity derivatives, operated as an exchange in South Africa from 1990 and the Bond Exchange of South Africa (Bond exchange) – trading bonds, was granted an exchange licence in 1996.

Both exchanges were acquired by the JSE in 2001 and 2009, respectively. LTX (www.a2x.co.za) currently already has no less than 88 listings.

A2X’s has far outperformed its rivals, EESE and 4AX. Of the total average number of daily transactions performed on the new exchanges in 2020, 56% of the transactions were made on A2X.

The competitive advantage A2X has over EESE and 4AX in attracting trades can be attributed to the linkage between A2X and the JSE, as stocks traded on A2X are already in issue on the JSE.

Thus, these stocks would be included in indices, and therefore be more liquid. EESE and 4AX are important for inclusive trading.

The two exchanges provide a platform on which small-cap companies may issue shares, and investors can trade a wider range of shares that are not exclusive to high-value stocks.

The upward and steady trend in the number of shares issued on all the newly registered exchanges reflects their essential role in providing a platform for listed firms to acquire liquidity for growth and expansion.

A listing on the NYSE will not suit most South African companies but for the select few the opportunity may prove well worth the effort and cost. It would however add another layer of trading opportunity for investors both locally and foreign.

Corrie Kruger is an independent analyst.

BUSINESS REPORT